Sanctions have backfired on those described by Vladimir Putin as the unfriendly nations. It is setting in train a series of events likely to undermine the whole Western financial system, as prices rise driving interest rates higher, and economic activity shrinks. These developments alone are leading to contracting bank credit, crashing stock markets, and sharply higher bond yields.

Last week, I wrote about the impact on the banking system and the likely consequences. Russia, China, and associated nations who depend upon them for trade and economic development are now moving to protect themselves from what is emerging as a full scale systemic and fiat currency crisis for the dollar and the entire Western financial system.

These developments are hastening the end of the petrodollar era and the dollar’s role as a reserve currency. A central Asian replacement is planned to be a new super-currency used for cross-border payments, based on an index of a basket of commodities and currencies of the participating nations. Including currencies is a mistake, but otherwise the proposition has merit.

This article explains why and how a properly constructed scheme would work. I demonstrate why it could act as a de facto gold standard.

Its designers intend this new trade currency to appeal to other important nations, such as Saudi Arabia, into using a commodity-linked currency for settling their trade payments, replacing the dying petrodollar. But its success could prove to be fatal for the fiat dollar and other Western currencies. With the demise of the dollar, the new super-currency can be expected to lead eventually to some national currencies adopting gold standards.

The ending of the petrodollar era

Put Ukraine to one side, it’s not the major issue. We should realise what really matters to us all is the real war, which is Russia’s attempts to banish American hegemony in Europe. While in the West we have an image of President Putin as an evil despot determined to take Ukraine back under Russian control, in a speech at St Petersburg’s International Economic Forum this week, Putin’s diagnosis of the West’s problems was more to the point than anything you will hear from our own Dear Leaders: Joe, Boris, Emmanuel, Olaf, et al. It is worth citing relevant extracts from the official English translation of Putin’s speech to highlight his economic understanding of the pickle we in the West have got ourselves into:

“Surging inflation in product and commodity markets had become a fact of life long before the events of this year. The world has been driven into this situation, little by little, by many years of irresponsible macroeconomic policies pursued by the G7 countries, including uncontrolled emission and accumulation of unsecured debt. These processes intensified with the onset of the coronavirus pandemic in 2020, when supply and demand for goods and services drastically fell on a global scale…

“Because they could not or would not devise any other recipes, the governments of the leading Western economies simply accelerated their money-printing machines. Such a simple way to make up for unprecedented budget deficits…

“I have already cited this figure: over the past two years, the money supply in the United States has grown by more than 38 percent. Previously, a similar rise took decades, but now it grew by 38 percent or 5.9 trillion dollars in two years. By comparison, only a few countries have a bigger gross domestic product. The EU’s money supply has also increased dramatically over this period. It grew by about 20 percent, or 2.5 trillion euros.

“Lately, I have been hearing more and more about the so-called – please excuse me, I really would not like to do this here, even mention my own name in this regard, but I cannot help it – we all hear about the so-called ‘Putin inflation’ in the West. When I see this, I wonder who they expect would buy this nonsense – people who cannot read or write, maybe. Anyone literate enough to read would understand what is actually happening.

“The rising prices, accelerating inflation, shortages of food and fuel, petrol, and problems in the energy sector are the result of system-wide errors the current US administration and European bureaucracy have made in their economic policies. That is where the reasons are, and only there.”[i]

Putin shows that he has at least a superficial understanding of where the West has erred with its neo-Keynesian monetary and economic policies. While some of the economic and monetary elements in his address can be criticised, Putin’s grasp of these subjects puts him head and shoulders above his opposite numbers in the G7.

It is from this disadvantage that the US is trying to impose dollar hegemony on Russian interests in the financial and currency war. We must consider the geopolitics of the matter.

Not that the West’s mainstream media tells it this way, but this is the story so far. Having chased the Americans out of Asia, the last failure being Afghanistan, Russia felt that there was one task remaining: to drive the Americans out of running Western Europe. Dominating the NATO alliance and with post-Brexit Britain no longer directly involved in the EU, the Americans were redoubling their efforts to contain Russia and hamper the Chinese-Russian partnership, which through the Shanghai Cooperation Organisation (SCO) is turning many of the West’s former allies away from America’s sphere of influence. As well as the oil-rich Middle East, most notable are India and Pakistan. Imran Khan led Pakistan increasingly closer to China, while India, notionally in the Commonwealth, was a longstanding client state of Russia for defence purposes and is now a member of the Shanghai Cooperation Organisation (SCO). Khan has now been deposed, allegedly by American interests which have reinstalled the previous regime.

China’s voracious appetite for commodities has made it the largest donor and influencer in sub-Saharan Africa and Central and South America. Brazil is increasingly involved with the SCO as a member of the BRICS group. Without many people noticing, between the SCO, BRICS, sub-Saharan Africa and Latin America, Russian-Chinese soft hegemony can now claim to influence states with well over half the world’s population.

Consequently, America’s hegemony is in decline. Yes, the dollar is still the international currency for pricing commodities and cross-border transactions, but the Eurasian Economic Union (EAEU) is designing a new commodity linked currency to be used as a medium of exchange between its members, and it is anticipated that this will be extended to all inter-SCO trade, SCO trade with non-member BRICS, and even with oil exporters in the Middle East.

Of particular concern for the Americans is the Middle East and Saudi Arabia. President Biden is due to visit in mid-July. And having flaunted his human rights credentials over the Jamal Khashoggi affair he has so far refused to say he is meeting the Saudis specifically. The Saudis say otherwise.

Now that US intelligence has openly blamed Khashoggi’s brutal death on direct instructions from Mohammed bin Salman (called MBS by nearly everyone on the diplomatic circuit), MBS has demonstrated he is ruthless. In seizing power, his disposal of all opposition from other members of the royal family was straight out of Machiavelli’s textbook written in admiration of The Prince — Cesare Borgia. How MBS deals with a weak, elderly US President who has all but insulted him, will be interesting to say the least. Let us just say that it is unlikely to go well for the American delegation.

Uppermost in Biden’s mind is likely to be oil supplies, and he will want to extract a promise that Saudi Arabia will increase its production to save America and her allies from the consequences of their own sanctions against Russia. It will be an uphill struggle, with MBS more drawn sympathetically to Vladimir Putin, getting on well with him. MBS runs Saudi Arabia in a similar fashion to Putin’s leadership in Russia.

When they high-fived each other at the November 2018 G20 meeting, the body language strongly suggests that they had a personal agreement between them which was going their way. It can only have been about cooperating on matters relating to their combined dominance of global energy markets the global oil markets. To get a sense of the body language between them, it is well worth watching that incident — twice. It can be found here.

At stake is the agreement President Nixon made with King Faisal in 1973, to sell oil exclusively for dollars, tying the Kingdom into the American banking system. It was an astute move by both parties at the time, allowing Sheik Yamani leading OPEC to raise the oil price from $3.56 per barrel more than tenfold over the next seven years, and to ensure the world needed dollars to pay for it. There can be little doubt that when Putin pulled the same trick on the EU with respect to oil payments in roubles, MBS would have noted the parallel with wry amusement.

The Arabs are not stupid. In 2014 I was told by the director of a major Swiss refinery that they were recasting gold bars for Arab customers from LBMA 400 ounces to the Chinese one kilo 9999 standard. It was the earliest indication I have had that the Arab nations in the Middle East were thinking their future lay more with China rather than the West. And there was no doubt that the Chinese had not only deliberately set out to become the largest gold mining nation, but they were moving to dominate the global physical market, ultimately threatening the LBMA standard.

So good luck to Joe Biden. Machiavelli wrote that

“A prince wins prestige for being a true friend or a true enemy. That is, for revealing himself without any reservation in favour of one side against another, this policy is always more advantageous than neutrality.”[i]

Given MBS’s track record and his apparent adherence to Machiavellian principals, the meeting with Biden will likely involve some straight talking. From MBS’s point of view, everything is stacked against the Americans. Biden is probably seen by him as a supplicant, which is associated with weakness. Honour, face, and public standing are what command respect in Arab culture, which will work against the Americans.

As infidels, the Americans have laid waste to Arab lands. But as well as a possible distaste for the Americans and their culture, MBS will also be considering his position vis-à-vis the Russian and Chinese axis, which has absorbed into itself Iran. On Russian encouragement, Iran has the power to harry shipping through the Straights of Hormuz. And though it has not yet made any headlines, the Houthis on Iranian instructions could step up their attacks on shipping in the Red Sea. It would be a natural response to Lithuania cutting off transport links to Kaliningrad this week in defiance of the treaty agreed between Lithuania and Russia in 1993.

The Saudis would have to think very carefully about the possible consequences of siding with the Americans in making promises it would not be in their interests to keep. It may be too early to say it with strong conviction, but the days of the petrodollar will probably be numbered when a viable Asian alternative becomes available. And the Saudis know it.

Replacing the petrodollar

The petrodollar’s strength has not just been its hegemonic status, but the relative weakness of commodity exporters’ currencies. Who, for example, would happily pay Indonesian rupiah for their copper exports — certainly not the Indonesians themselves who would prefer dollars.

Nearly all international accounting is in dollars, which means that the easiest decision for any international trader is to simply maintain dollar balances. It is for this reason that foreign ownership of dollar financial assets and bank balances now exceeds $33 trillion, almost one and a half times US GDP. That is a hard act to follow.

Under Western sanctions and without access to dollars, the Russians have said they would be content to trade in national currencies. For them, accepting even Turkish lira — probably a worse currency than Indonesia’s rupiah — is preferred to any of the “unfriendlies’” currencies, which are currently worthless in Russia’s hands. But this can only be a temporary arrangement. Consequently, the Russians are looking for a better solution.

Presumably, Putin will not want to see the rouble exposed to manipulation by Russia’s enemies. And he will have gamed various scenarios for ending the dollar’s hegemonic status, or at least undermining its credibility which will have alerted him to potential dangers for Russia’s currency. That being so, he won’t want to see potentially destabilising balances of roubles accumulate in foreign hands. To a statist like Putin free markets for his currency are likely to be considered potentially dangerous.

Assuming therefore that Russia wishes to maintain at least some exchange controls, there are two separate issues: there is the currency to replace the dollar required for cross-border trade settlements which can be freely converted into roubles by the state and Russian commercial interests, thereby limiting the build-up of foreign-owned roubles available on the foreign exchanges; and there is that of the domestic rouble itself. In common with other Asian nations, government control over their domestic currencies is unlikely to be sacrificed easily.

Plans for a trade settlement currency are already advancing under the aegis of the Eurasian Economic Union (EAEU), a project being developed by Sergey Glazyev. Glazyev is Russia’s Minister in charge of integration and macroeconomics of the EAEU. While planning to do away with dollars for trade settlements has been in the works for some time, sanctions by the unfriendlies against Russia have brought about a new urgency.

We know little detail, other than which was revealed in an interview Glazyev gave recently to a media outlet, The Cradle[ii]. The new trade currency will be entirely comprised of credit balances at both central and commercial banks, presumably price-fixed daily, giving conversion rates into local currencies. The central banks of participating states can create the new currency by buying in their own currencies from importers and exporters for conversion. Other than the proposed inclusion of national currencies in the basket, it is a practical concept. It is probably the reason the Kremlin is said to be considering it as an option for backing the rouble in future.

That idea of a commodity basket for the rouble itself is likely to be abandoned as unnecessary, while a successful EAEU trade settlement currency can be extended from EAEU nations to both those in the wider SCO and the BRICS members not in the SCO. It could also be an acceptable replacement of the petrodollar for oil export payments to the Middle East.

The ambition is for it to become the mechanism for freeing over half the world from dollar hegemony, including all nations whose export markets now depend more on Asia than the current developed world. In October 2020, the original motivation was explained by Victor Dostov, president of the Russian Electronic Money Association:

“If I want to transfer money from Russia to Kazakhstan, the payment is made using the dollar. First, the bank or payment system transfers my roubles to dollars, and then transfers them from dollars to tenge. There is a double conversion, with a high percentage taken as commission by American banks.”

Having originally had a practical element to it, the motivation for change has now become politically urgent due to Western sanctions.

The problems with Glazyev’s proposals

In his interview with The Cradle, Sergey Glazyev described the new trade currency for the EAEU as being comprised of a weighted index of the currencies of participating nations, bolstered by up to twenty exchange-traded commodities. It is the inclusion of currencies which is bound to cause difficulties. For example, Glazyev said China’s yuan would not be included “due to its inconvertibility and the restricted external access to the Chinese capital markets”. But Russia has also introduced strict exchange controls in the wake of Western sanctions, and one can envisage other member states wanting the freedom to do so as well if they haven’t already done so. The simple and obvious solution is not to include currencies at all. If it is to be used solely for international trade, then there is no reason to include them. And by not involving them, any country simply prepared to exchange its own currency for the new trading unit can join. It becomes a simple one-page agreement.

The objective is to bypass the dollar. To do that successfully, the new trade currency must be a better medium of exchange and store of value than the dollar to encourage the businesses of participating nations to hold deposits in it in preference to the dollar. Simplicity in its construction and transparency in its composition are key. And certainty that its administrators are not going to alter its composition without good reason will be important for anyone considering migrating trade settlements from dollars. This rules out weighting commodities in an index as well because it is only the aggregated prices that matter.

It is clear from the Cradle interview that Glazyev errs badly in his approach. He is muddling a political imperative to conflate domestic currency considerations with those of international trade. Yet he acknowledges that the nature of the proposed currency should permit participating nations to manage their own currencies as they see fit. If that’s to be the case, then it’s a further reason why they are not suited for inclusion.

It is hardly surprising that introducing national currencies and possibly weighting them based on national GDPs, as Glazyev suggested, is making it difficult to come to an agreement. Glazyev admits planning for this new currency started ten years ago, when it could have been done and dusted in an afternoon by someone who knew what he was doing. As an excuse, politics is lame. Make a properly considered proposal for a simple clear structure and either nations sign up to it or they don’t.

Furthermore, Glazyev’s comment that “The use of gold as the price reference is constrained by the inconvenience of its use for payments” exposes an appalling lack of knowledge about money. Gold very rarely circulates as money, almost always hoarded as the last and not the first means of payment. It is credible substitutes for gold that circulate. Any fiat currency can be turned into a gold substitute by an issuer prepared to exchange its currency on demand on pre-agreed terms. Glazyev should have known this.

Nevertheless, so long as a commodity-based currency is used and accumulated only for cross-border transactions, it can be a practical proposition. The appropriateness and durability of a properly constructed supranational currency for trade purposes is our next topic.

How durable will a commodity-based trade currency be?

The long-term success of any currency depends on its stability — stability in terms of its purchasing power and acceptability as a medium of exchange, values which have been lost in the fiat dollar-centric world.

In the planning of such a currency there are issues to be addressed. Such a currency is a creature of government and not its users, so its users must be satisfied with its properties and credibility. For a commodity-based currency to operate, it must be supplied by participating central banks in return for buying in their own currencies. Thus, an exporter paid in a local currency can convert it immediately into the new super-currency. Or an importer can buy it from its central bank on payment of local currency. These transactions can be routed through commercial banks having deposit accounts with their central bank.

For these transactions to take place require daily, or even twice-daily fixings indexed in all participating currencies.

The only transactions involving dollars will be conducted directly with commodity exchanges and suppliers not in the scheme, so cannot be settled in the new trade currency. For it to be otherwise the US authorities would have to be included in the scheme and the participating members would probably veto that anyway. But non-American banks prepared to issue and deal in offshore dollar credit and domiciled in a participating nation would be able to do so. The most likely candidates for this trade would be the Chinese banks, and import/export banks or divisions of banks established for the purpose. Currency hedging facilities and associated instruments would probably evolve in secondary markets where there is demand for them. And when a commodity exporter seeks settlement in the new trade currency it would be done with reference to the buyer’s currency, converted by the national central bank at the daily fix into the new trade currency.

Designing the new currency

Given Glazyev’s interview with The Cradle, we cannot say for sure that these issues will be credibly addressed. But we can assess the likely success of a commodity-based currency which is properly designed.

It must work as if it is a gold substitute. Unlike many of their Western counterparts, Eurasian traders and consumers have not forgotten that gold is money. And while a pure gold standard would be the simplest and best solution by far, the likelihood of a new statist currency succeeding must be measured against the people’s preferred money —gold.

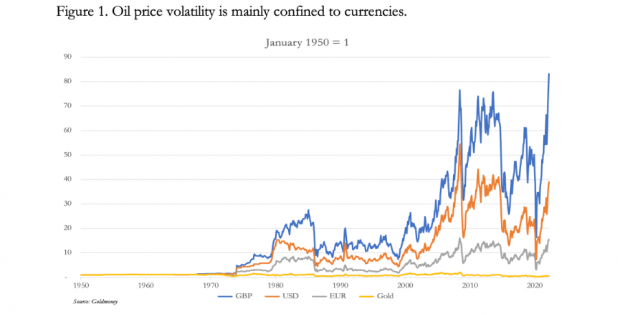

Russia is the world’s largest exporter of energy and given that the EAEU’s new monetary committee is run by a senior Russian, we can expect the oil price to be included in the commodity basket. Furthermore, energy is the most fundamental of all commodities. The history of oil prices provides a guide to the challenges to be addressed by its inclusion. Figure 1 shows the oil price in three major currencies and priced in gold from 1950.

In sterling, the price of oil has soared 83 times since 1950, in dollars 39 times, in euros (and before 2000 in relatively stable Deutsche marks) 15 times. If euros in their current form had existed earlier, we can be sure that the oil price in euros would have risen far more.

In gold, the price has fallen 30%. Knowing that sound money is gold, and the currencies are backed by nothing more than faith and credit in the issuing governments, it is noticeable how nearly all the price volatility is not in oil itself, but in the currencies.

This cuts across the basic understanding that in any economic transaction where a medium of exchange is used, all price objectivity should be in the medium of exchange and all price subjectivity is in the goods or services being exchanged. For the parties in a transaction, even though a seller of goods prefers currency to the goods and the buyer prefers the goods to the currency, they can both agree that a dollar is a dollar, and any variation in value is confined to the goods.

Investment and industry analysts never question the objectivity of currencies, assuming all predicted price changes are in the investment or commodity analysed. Even technical analysts with their charts fall into this trap. Readers of this nonsense usually expect to be given price forecasts. And the answer is always based on an assessment of expected supply and demand for XYZ, and never ever couched in these more correct terms: “We can model the likely changes in supply and demand for XYZ, but cannot forecast price effect because we don’t know how the currency might change over time.”

The origin of price objectivity in the currency and price subjectivity in goods and services stems from the economic theory of marginal pricing formulated by Carl Menger in the 1870s and subsequently developed by Austrian economists. Being fully exchangeable for gold coin, currencies at that time took on the characteristics of money proper, and Menger’s findings describe the relationship between sound money and goods, which was valid for currencies on a credible gold standard. With the abandonment of all forms of gold backing in 1971, fiat currencies became free to vary in purchasing power. While participants in transactions believe the objective/subjective relationship under a gold standard is still the case today, there is an additional chapter yet to be written on price theory as Figure 1 above demonstrates.

Until that is done, everyone remains unconsciously wedded to the gold standard’s pure objective/subjective relationship with respect to fiat currencies. But then the general understanding of catallactics (the theory of exchange ratios and economics of prices) was never that great anyway and has almost vanished following the Keynesian revolution.

The value of one commodity, good, or service will vary against those of the others depending on relative demand for it. Therefore, under the artificial condition of no change in the quantity of money, currency, and credit and assuming there is no change in the propensity of the population of consumers and producers in aggregate to retain their available liquidity, some prices will rise, and others fall. Even then, we still cannot claim, as Leon Walrus of the Lausanne school attempted, that the whole pricing system equilibrates. But there is no doubt that not only do values of commodities vary against each other, but a basket of them represented in an index can be expected to be a relative stable measure of purchasing power as experience with the gold price of oil suggests.

This is why metallic money is fundamentally sound. Over the millennia gold, silver, and copper have proved to be the best forms of media of exchange. And gold, with its durability, restricted quantity, and the fact that it is not consumed, emerged as the preferred money standard in the nineteenth century. It is said that its purchasing power for common items in Roman times is similar to their equivalents today. And this is certainly evident from Diocletian’s edict on prices issued 1,700 years ago.

In Figure 1 above, that the gold price of oil has varied little from 1950 to the current day confirms that the objectivity of prices in gold is a valid argument, while measured in fiat currencies it is not. We can go further and illustrate the point in other commodities. Figure 2 shows the end of year prices of copper in dollars and gold.

That copper has become 70% cheaper in sound money over the last 120 years makes sense. While demand has increased, it has seen supplies increase as well. New deposits have been found, and the extraction costs per unit of output have fallen as mining methods and technological improvements have developed. These have more than supplied demand for new uses for the metal.

As a commonly used metal, demand for copper is widely acknowledged as a forward indicator of overall economic conditions. Doctor Copper is so named. As crude oil is to energy, copper is to base metals.

Figure 3 shows prices for scrap iron and steel, central to construction and other basic industries.

Since 1934, scrap prices have risen 69 times in dollars, but only 32% in gold. Again, the chart confirms that for a key material, priced in sound money it is little changed over nearly ninety years.

We can see from only three key components that a basket of commodities used for determining the exchange rate for a new trade currency will ensure the currency retains its purchasing power over time and can be expected to act as a far better trade or reserve store of value than the fiat dollar. It would be the closest equivalent to a gold substitute without the involvement of gold itself. If such a currency becomes properly established, then irrespective of US monetary policies the dollar is likely to be discarded for trade settlement purposes between the nations in the EAEU, the SCO, Brazil as the non-Asian BRICS participant, and potentially all their commodity and trade counterparties in Africa South America, and the Middle East.

The strength of such a scheme is that the trade currency would be chosen by its users in preference to the dollar — the commodity suppliers, manufacturers, and import-exporters — not their governments. The American hegemonic practices of leaning on governments and organisations such as OPEC to only trade in dollars would no longer work.

But the success of a new trade currency raises a question over the future of the $33 trillion of foreign-owned US financial assets and deposit balances. If the scheme gets off the ground successfully, the impact on the dollar will almost certainly be for foreign interests to unwind these assets substantially, to replace them with balances in the new trade currency. Foreign-owned capital would be withdrawn from the US economy in devastating quantities.

A further question is then raised over the common practice of pricing all commodities in dollars. A new trade currency indexed to commodities but whose only exchange value is with currencies of the issuers signed up to participate cannot easily be used to price individual commodities on a continual basis. So long as the dollar’s credibly exists, prices are likely to continue to be set in dollars. But the superiority of a properly constructed trade currency can be expected to undermine the dollar’s purchasing power to the extent that markets are likely to finally abandon it as an objective means of commodity value. The solution is obvious: the best medium of exchange for commodity pricing purposes is gold itself, even if represented by a credible currency and credit substitute.

It is hard to conclude otherwise. A trade currency based on a basket of goods is, in effect, a means of reintroducing gold as the money-standard in which all commodities are priced. It will encourage fiat currencies everywhere to be converted into credible gold substitutes to survive.

The financial war— the endgame

This article commenced with the assertion that the real war between Russia and the West is financial in nature, and it has attempted to explain why. Nevertheless, there are many loose ends to consider.

Perhaps the greatest hurdle Putin must overcome (and for that matter Xi in China) is the intellectual corruption of his advisers, who have adopted many of the West’s economic and monetary fallacies. Glazyev’s poor comprehension of catallactics has been pointed out. And in his speech in St Petersburg, Putin referred to economic growth. This is not the same as what users of the term growth think it means, which is economic progress, and is a common error.

Misled by Western macroeconomics, it is likely that Putin’s advisers will caution against an exchange rate tied to commodities as being too strong, undermining the export trade. Perhaps it is this error which leads Glazyev to attempt to soften the proposed trade currency by including currencies. Even worse, Keynesian-style economic stimulus is almost certainly believed in by Russia’s Western-influenced monetary policymakers.

The best that can be hoped for is that by planning to introduce a new commodity-based international trade currency on the lines described above, Russian, and Chinese economic advisers, understand it allows them to retain the so-called benefits of currency and interest rate economic management for their domestic economies.

Perhaps they will not see that the dollar’s destruction by establishing a successful commodity-based trade currency will permit gold standards to creep in through the back door.

—

[i] It is worth reading in full the official translation of Putin’s speech, which can be found here: http://en.kremlin.ru/events/president/news/68669

[iI] The Prince, Niccolo Machiavelli, XXI — “How a Prince must act to win honour”.

[iiI] https://thecradle.co/Article/interviews/9135

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated.

Copyright © Goldmoney Inc

https://www.lewrockwell.com/2022/06/alasdair-macleod/russia-is-winning-the-financial-war/