This concentration of housing ownership by the wealthy is the direct result of Federal Reserve and federal policies that benefit the wealthy.

We're told that sky-high rents and home prices are the result of a shortage of housing. The solution is simple: build more housing.

This sounds obvious, but the reality is the problem isn't a shortage, it's the concentration of housing ownership in the top 10%, the same 10% who own the majority of other income-producing assets like stocks and bonds.

The problem is the wealthy are hoarding housing as just another income-producing asset to accumulate because the central bank / economic-financial policies of the past few decades have favored capital over labor and the already-wealthy who bought assets when they were cheap.

The trillions of dollars in new credit have been asymmetrically distributed: the most creditworthy with the highest incomes and collateral are the top 10%, so they scooped up most of the credit. Since real estate is so heavily dependent on credit (20% down and 80% borrowed, not like stocks and bonds), this massive influx of low-cost credit led to the top 10% accumulating investment housing.

In other words, the asymmetric distribution of credit concentrated ownership of housing in the hands of the few at the expense of the many. The wealthy entered bidding wars for "surplus housing" with other wealthy, a bidding process based largely on who had access to the lowest-cost credit and whose existing wealth had ballooned up more in the central bank-generated Everything Bubble.

Those without existing credit-bubble-collateral or the free money issued by the Bank of Mom and Dad couldn't compete.

Given these asymmetries in credit, collateral and family wealth, there was no way the wealthy wouldn't end up with the lion's share of "surplus housing," just as they ended up owning the lion's share of stocks, bonds, precious metals, cryptocurrencies, artwork, etc.

There are many sources of housing-hoarding. One is inheritance. The parents move into assisted living or pass on, and since the family was wealthy enough to help the kids buy their own homes at an early age, the parent's home is "surplus capital" that stays in the family.

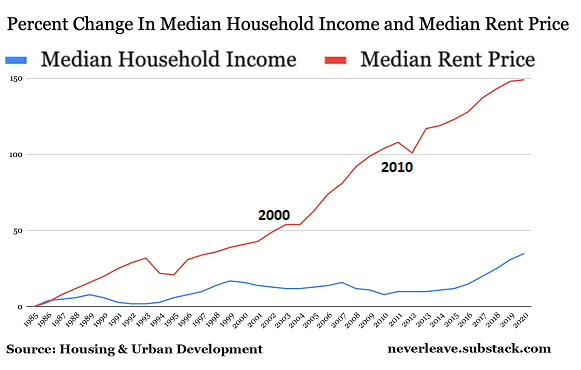

Another is corporate buying of rental properties. Steadily rising rents (see last chart below) make rental housing a low-risk, attractive investment, so corporations tapped their credit lines or the corporate bond market to snap up tens of thousands of rental homes. Since corporate costs of capital and management are lower than those available to households, corporations can afford to be less price sensitive. Individual buyers could be outbid by corporations.

A third source is the recent "investment craze" for short-term vacation rentals (STVR) as the wealthy heard stories of other wealthy people getting $10,000 a month from homes that fetched $2,000 a month as long-term rentals.

This differential unleashed a tsunami of home purchases by the wealthy seeking to maximize their gains on cheap credit and "excess capital" stagnating in their accounts earning near-zero interest.

In classic fashion, this land-rush frenzy to capture the outsized profits from STVR gobbled up all the housing inventory, creating credit-induced scarcity. Also in classic fashion, wealthy bidders began basing their bids not on $3,000 a month via long-term rental income, but $12,000 a month (in peak season) income from price-insensitive tourists via STVR.

The deluge of "revenge spending" unleashed after the pandemic lockdowns ended supercharged the greed and acquisition of housing for short-term vacation rentals. $12,000 a month was now chump-change; the price jumped to $15,000, and soon enough, this was a "bargain" that needed another boost higher.

Those desperate for vacations regardless of cost were the perfect customer base for rampant price-gouging, a.k.a. "maximizing return on investment."

The true scale of this land-rush by the wealthy into STVRs is difficult to assess for various reasons. To get preferential mortgage and property tax rates, some new owners may have claimed residency or listed the new purchase as a second home. The only way to accurately assess the true scale is to tote up STVR licenses in locales that require STVR owners to obtain permits and pay annual registration fees.

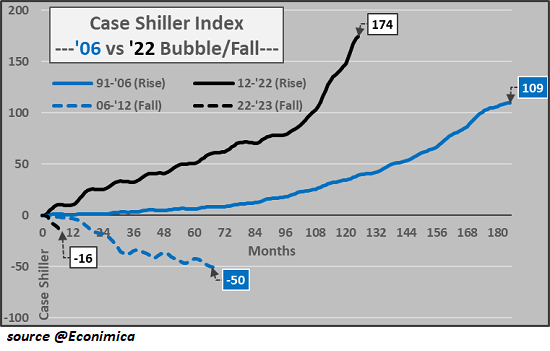

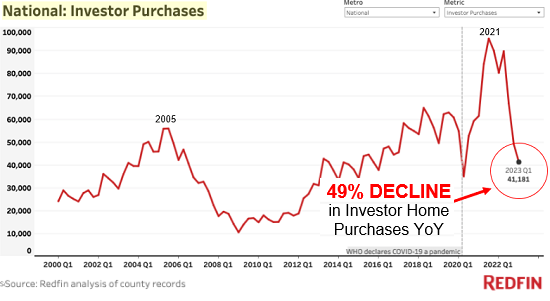

Consider the facts displayed below. The current housing bubble arose as a direct result of the flood of stimulus issued by the Federal Reserve and Treasury post-pandemic. Note the massive spike in investment purchases that resulted.

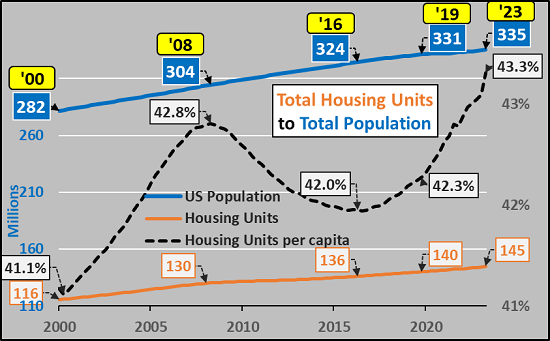

The third chart shows that the US population rose by 4 million 2019-2023 while housing expanded by 5 million units. Um, OK, where is the scarcity when housing per capita (per person) is at record highs?

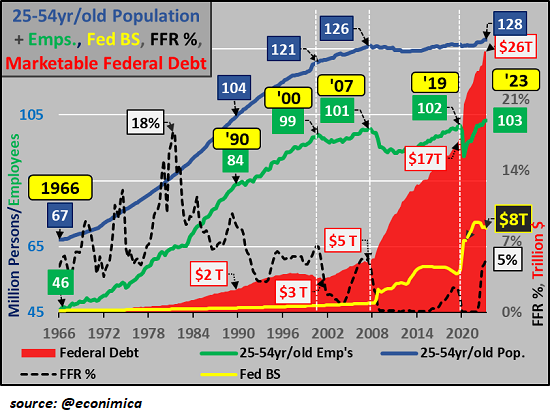

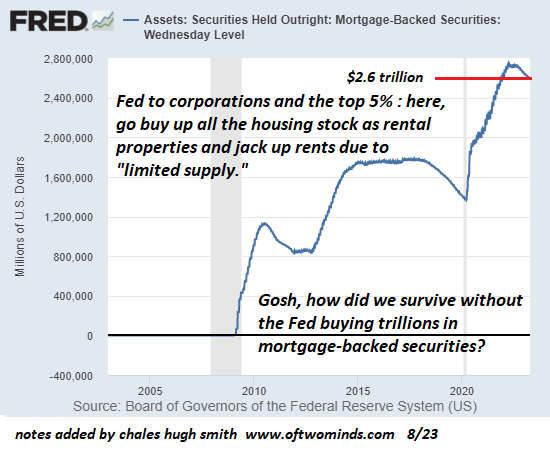

The fourth chart shows that the prime home-buying cohort (ages 25-54) has flatlined since 2008, along with the number employed and thus able to obtain and pay a mortgage. What skyrocketed wasn't the number of employed home buyers--what skyrocketed was credit and central bank / government stimulus: the Fed balance sheet and holdings of mortgage-backed securities skyrocketed (fifth chart), directly goosing housing via lowering mortgage rates, and federal deficit spending.

The wealthy are hoarding housing because the system has incentivized dumping "excess capital and credit" into housing. This concentration of housing ownership in the wealthy is the direct result of Federal Reserve and federal policies that benefit the wealthy.

As longtime correspondent Suzanne S. put it: "I'm not sure we have a housing crisis as much as an ownership crisis."

https://www.oftwominds.com/blogaug23/hoarding-housing8-23.html?fullweb=1

https://www.oftwominds.com/blogaug23/hoarding-housing8-23.html?fullweb=1