During Friday’s bloodbath, I heard a CNBC anchor lady

assuring her (scant) remaining audience that Brexit wasn’t a big sweat.

That’s because it is purportedly a politicalcrisis,

not a financial one.

Presumably in the rarified canyons of Wall Street, politics

doesn’t matter much. After all, when things get desperate enough, Washington

caves and does “whatever it takes” to get the stock averages moving upward

again.

Here’s a news flash. That’s all about to change.

The era of Bubble Finance was enabled by a political

abdication nearly 50 years ago. But as Donald Trump rightly observed in

the wake of Brexit, the voters are about to take back their governments,

meaning that the financial elites of the world are in for a rude awakening.

To be sure, the apparent lesson of the first TARP

vote when the bailout was rejected by the House in September 2008 was that

politics didn’t matter so much.

Wall Street’s 800 point hissy fit was all it took to prostrate

the politicians. Indeed, the presumptive free market party then

domiciled in the White House quickly shed its Adam Smith neckties and forced

the congressional rubes from the red states to walk the plank a second

time in order to reverse the decision.

There was a crucial predicate for this classic crony

capitalist capture of the authority and purse of the state, however, that

should not be overlooked. Namely, that in the mid-cycle period of the world’s 20-year experiment in central bank

driven Bubble Finance the rubes had not yet come to fully appreciate that they

were getting the short end of the stick.

Indeed, the earlier phases of the bubble era witnessed an

enormous inflation of residential housing prices. For instance, between

Greenspan’s arrival at the Fed in August 1987 and the housing bubble peak in

2007, the value of residential housing rose from $5.5 trillion to $22.5 trillion or by 4X.

The greatest extent of the housing bubble occurred in the

bicoastal precincts, of course. But it did lift handsomely the value of 50

million owner-occupied homes in the flyover zone, as well.

Accordingly, the latter did not yet see that the

new regime was stacked in favor of the top 10% of the economic

and wealth ladder, which owns 85% of the non-housing financial assets. And

that the speculative casinos of Bubble Finance would be an especially

verdant source of windfalls for the top 0.1%.

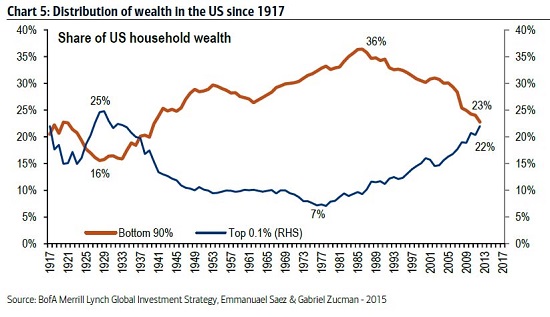

Indeed, the

entire 13 percentage points of the wealth pie lost by the bottom 90% of

households (105 million households) during the past 30 years have been

captured by the 120,000 households at the tippy-top (0.1%).

Nor was it yet evident as to the degree to which massive

money printing under conditions of Peak Debt almost exclusively

stimulates Wall Street speculation, not main street production, jobs, incomes

and spending.

In any event, by the eve

of the great financial crisis, the GOP was actually controlled by the

racketeers of the Beltway and the Wall Street gamblers, not the red state

voters who had elected it.

In fact, Goldman’s Sach’s plenipotentiary to Washington,

Hank Paulson, was in complete command of the elected side of

government. At the same time, the Bush White House had populated

the central banking branch of the state with proponents of monetary activism,

who were more than ready to authorize “heroic” measures to reflate the bubble.

Needless to say, the leader of the pack, Ben Bernanke, had been

groomed for the role of chief bailster by none other than Milton Freidman. The

latter, in turn, had led Nixon astray at Camp David 37 year earlier when

he persuaded Tricky Dick to default on the dollar’s link to gold,

thereby opening the door to fiat money, massive credit expansion and the

modern era of Bubble Finance.

There is a straight line of

linkage from that great historical inflection point to Friday’s Brexit

uprising. Namely, Nixon’s abandonment of the Bretton Woods gold-exchange

standard, as deficient as it had been, was also a profoundly political

act.

It resulted in the abdication of economic and financial

policy to an unelected elite and their eventual capture by Wall Street and the

forces of speculation and financialization unleashed by unanchored central bank

money and credit.

Nixon’s destruction of Bretton Woods was the enabling

event. It turned central bankers and financial officialdom loose to

operate a dictatorship of bailouts, bubbles, and financialization of

economic life. And to spread this baleful regime to Europe, Japan and the

rest of the world, too.

To be sure, it took more than two decades to fully

materialize. There were deeply embedded institutional cultures and ideologies

among policy-makers that restrained opened-ended resort to the printing press

and financial bailouts.

The Paul Volcker interlude in the US and the determined sound

money regime of the Bundesbank are cases in point.

But eventually, the old regime gave way. There emerged

Greenspan’s dot-com and housing bubbles, the rise of the ECB and

the financial rulers of Brussels, the massive bailouts triggered by

the global crisis of 2008-2009, the hideous expansion of central bank

balance sheets during the era of QE and ZIRP, the emergence of

the destructive “whatever it takes” regime of Draghi and the

current financial lunacy of subzero interest rates across much of the planet.

But here’s the thing. The rubes are on to the rig.

Twenty-years of Bubble Finance have made the City of London an

oasis of splendor and prosperity, for example, but it has left the

hinterlands of Britain hollowed-out industrially, resentful of the

unearned prosperity of the elites and fearful of the open-ended flow

if immigrants and imports enabled by the superstate in Brussels. As on

observer put it, the geography of the vote said it all:

“If you’ve

got money, you vote in,” she said, with a bracing certainty. “If you haven’t

got money, you vote out.” We were in Collyhurst, the hard-pressed neighbourhood

on the northern edge of Manchester city centre last Wednesday, and I had

yet to find a remain voter.

Look at the map of those results, and that huge island of “in”

voting in London and the south-east; or those jaw-dropping vote-shares for

remain in the centre of the capital: 69% in Tory Kensington and Chelsea; 75% in

Camden; 78% in Hackney, contrasted with comparable shares for leave in such

places as Great Yarmouth (71%), Castle Point in Essex (73%), and Redcar and

Cleveland (66%). Here is a country so imbalanced it has effectively fallen

over.”

The rise of Trumpism in the US reflects the same social and

economic fracture. To wit, Bubble Finance has also drastically unbalanced the

US as between the bicoastal zones of prosperity it has enabled and the

fly-over zones its has effectively left behind.

It goes without saying that massive debt monetization and

90 months of zero interest rates has been a boon for the Imperial City. With

almost, no restraints on its ability to borrow and spend, the

military/industry/security/surveillance complex have prospered like never

before, as has the medical care cartel, the education syndicate and the lesser

beltway rackets such as green energy and the farm subsidy/food

stamp/ethanol alliance.

Likewise, asset gatherers, financial intermediaries, brokers,

punters, financial engineers and corporate strip-miners have prospered

enormously because the market has been rigged every since Black Monday in

October 1987. That is, the cost of debt and carry trades have been

falsified, downside hedging insurance in the casino has become dirt cheap

and time after time the Fed’s put has bailed-out speculations gone bust.

Even what passes for entrepreneurial breakouts in the world

of social media and new tech isn’t really. It’s just another variant of the

dot-com bubble in which a few good innovations are being drastically

over-valued (e.g. Uber) while a tsunami of worthless and pointless

start-ups have become giant cash burning machines (e.g. Tesla).

Taken all together, they are funding an ephemeral complex

of pseudo businesses, pseudo jobs and pseudo start-up networks that

are attracting tens of billions in venture capital. But that amounts to a

simulacrum of prosperity today and the substance of

tomorrow’s malinvestment waste and losses.

Meanwhile, the main street economy has atrophied. The first

round of Bubble Finance buried the middle class in debt, while the post-crisis

intensification has turned the C-suites of America into a giant stock trading

room and financial engineering arena.

Contrary to the bubble vision pattern, in fact, there has been

no business deleveraging at all. On the eve of the crisis in Q4 2007, total

non-financial business debt outstanding was $11 trillion, and it is now $13.5

trillion.

But on the margin, every dime of that massive swelling of the

business debt burden represents real economic resources cycled out of the

flyover zones and pumped back into the financial casinos and the bicoastal

elites which fatten on them.

The recent studies of the Census Bureau data which show that just 20 counties have generated

half of all start-ups since the financial crisis provides another take on the

underlying fissure. What the study describes but doesn’t explicitly articulate

is that the massive flow of venture capital to the 20 mainly bicoastal counties

and outposts of the military/industrial/security/surveillance state is itself a

product of Bubble Finance:

Americans in small towns and rural communities are dramatically

less likely to start new businesses than they have been in the past, an

unprecedented trend that jeopardizes the economic future of vast swaths of the

country.

The

recovery from the Great Recession has seen a nationwide slowdown in the

creation of new businesses, or start-ups. What growth has occurred has been

largely confined to a handful of large and innovative areas, including Silicon

Valley in California, New York City and parts of Texas, according to a

new analysis of Census Bureau data by the

Economic Innovation Group, a bipartisan research and advocacy organization that

was founded by the Silicon Valley entrepreneur Sean Parker and small group of

investors.

That concentration of start-up activity is unusual, economists

say. In the early 1990s recovery, 125 counties combined to generate half the

total new business establishments in the country. In this recovery,

just 20 counties have generated half the growth.

The data suggest highly populated areas are not adding start-ups

faster now than they did in the past; they appear simply to be treading water.

But rural areas have seen their business formation fall off a cliff.

Economists say the divergence appears to reflect a combination

of trends, all of which have harmed small businesses in rural America. Those

include the rise of big-box retailers such as Walmart, the loss of millions of

manufacturing and construction jobs across the country and a pullback in

business lending that appears to have stung small-town and rural borrowers

particularly hard.

The changes also reflect a fundamental shift over the past two

decades in which workers and industries power the country’s economic growth.

That shift advantages highly educated urbanites at the expense of everyone

else. Polling suggests it is one of the driving forces in the political unrest

among working-class Americans — particularly rural white men — who have flocked

to Republican Donald Trump’s presidential campaign this year.

In short, Bubble Finance is a giant engine of reverse Robin Hood redistribution.

It embodies a sweeping fiscal intervention in the natural flows of the

free market that punishes savers, laborers, self-funded main street

entrepreneurs and the retired populations in favor of speculators, the holders

of existing financial assets and the dealers in money.

Bubble Finance is an affront to both democratic governance and

true capitalist prosperity. The Trump voters, the Brexit voters, the

masses rallying to the populist banners throughout Europe above all else

represent a reactivation of the political machinery in a last-ditch campaign to

stop the financial elites and their regime of Bubble Finance.

Yes, this time is different, and this time, there will be no

reflation of the financial bubble like there was after Black Monday, the S&L

bust, the dot-com crash and the great financial crisis of 2008-2009.

Needless to say, the Wall Street dip-buyers and perma-bulls who

take their cues from the modern day financial ruling class are in for a shock.

And today’s statement by Martin Schulz, the President of the EU

parliament could not more aptly explain why.

Said Schulz,

“The British have violated the rules. It is not the EU philosophy

that the crowd can decide its fate“.

We think Schulz is dead

wrong.