A recent article out this past week by Russ Koesterich via BlackRock noted that bond yields had not melted-up as “everyone expected.”

Sorry, Rick.

It’s not everyone, just you guys on Wall Street.

Since 2013, I have been laying out the case, repeatedly, as to why interest rates will not rise. Here are a few of the most recent links for your review:

- April 20, 2017 – Why Bonds Aren’t Overvalued

- March 23, 2017 – The Long View – Rates, GDP & Challenges

- October 24, 2016 – End Of The Bond Bull, Better Hope Not

- August 30, 2016 – Why Interest Rates Are Going To Zero

- August 27, 2016 – Let’s Be Like Japan

As I said, I have been fighting this battle for a long-time while “everyone else” has remained focused on the wrong reasons for higher interest rates. As I stated in “Let’s Be Like Japan:”

“Yellen has become caught in the same liquidity trap as Japan. With the current economic recovery already pushing the long end of the economic cycle, the risk is rising that the next economic downturn is closer than not. The danger is that the Federal Reserve is now potentially trapped with an inability to use monetary policy tools to offset the next economic decline when it occurs.This is the same problem that Japan has wrestled with for the last 20 years. While Japan has entered into an unprecedented stimulus program (on a relative basis twice as large as the U.S. on an economy 1/3 the size) there is no guarantee that such a program will result in the desired effect of pulling the Japanese economy out of its 30-year deflationary cycle. The problems that face Japan are similar to what we are currently witnessing in the U.S.:

- A decline in savings rates to extremely low levels which depletes productive investments

- An aging demographic that is top heavy and drawing on social benefits at an advancing rate.

- A heavily indebted economy with debt/GDP ratios above 100%.

- A decline in exports due to a weak global economic environment.

- Slowing domestic economic growth rates.

- An underemployed younger demographic.

- An inelastic supply-demand curve

- Weak industrial production

- Dependence on productivity increases to offset reduced employment

The lynchpin to Japan, and the U.S., remains interest rates. If interest rates rise sharply it is effectively “game over” as borrowing costs surge, deficits balloon, housing falls, revenues weaken and consumer demand wanes. It is the worst thing that can happen to an economy that is currently remaining on life support.”

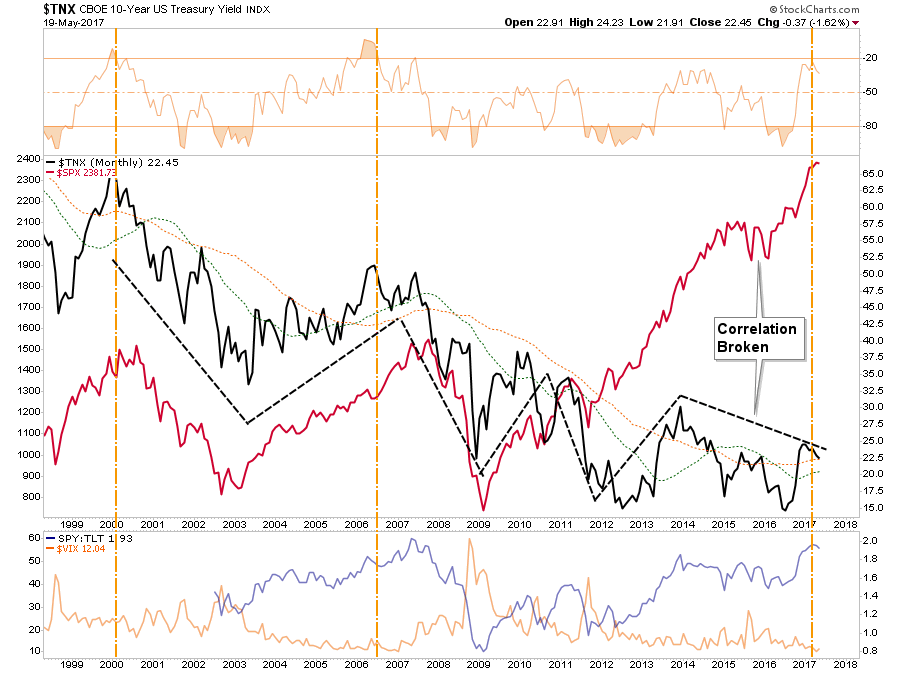

While Central Banks continue to intervene where possible to support asset prices, the recent decoupling of the market from the underlying rate structure, in hopes of “Trumponomics,” is likely transient. The only question is simply how long it will be before “reality” and “hope” reconnect.

The last time the stock/bond ratio (purple line) was this elevated, it didn’t work out well for investors as volatility spiked, equity prices plunged and the “sprint for safety” send bond prices surging.

Unfortunately, the Fed is still misdiagnosing what ails the economy and monetary policy is unlikely to change the outcome in the U.S., just as it failed in Japan. The reason is monetary interventions, and government spending, don’t create organic, and sustainable, economic growth. Simply pulling forward future consumption through monetary policy continues to leave an ever growing void in the future that must be filled. Eventually, the void will be too great to fill.

But hey, let’s just keep doing the same thing over and over again, which hasn’t worked for anyone as of yet, hoping for a different result.

What’s the worst that could happen?