There are no extreme "fixes" to secular declines in

sales, profits, employment, tax revenues and asset prices.

The saying "never let a

crisis go to waste" embodies several truths worth pondering as the stock

market nears new highs. One truth is that extreme policies that would raise

objections in typical times can be swept into law in the "we have to do

something" panic of a crisis.

Thus wily

insiders await (or trigger) a crisis which creates an opportunity for them to

rush their self-serving "fix" into law before anyone grasps the

long-term consequences.

A second truth is that crises

and solutions are generally symmetric: a moderate era enables moderate solutions, crisis eras

demand extreme solutions. Nobody calls for interest rates to fall to zero in

eras of moderate economic growth, for example; such extreme policies may well

derail the moderate growth by incentivizing risk-taking and excessive leverage.

Speculative credit bubbles

inevitably deflate, and this is universally viewed as a crisis, even though the

bubble was inflated by easy money, fraud, embezzlement and socializing risk and

thus was entirely predictable.

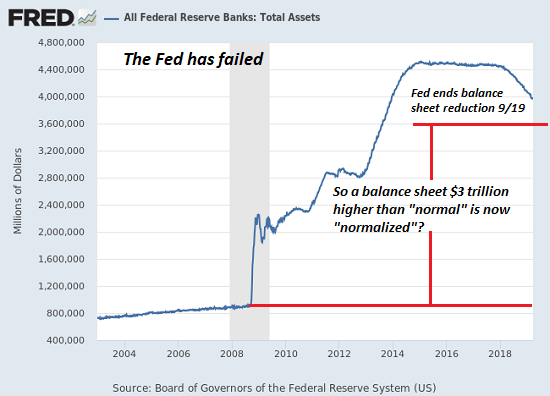

The Federal

Reserve and other central banks are ready for bubble-related financial crises:

they have the extreme tools of zero-interest rate policy (ZIRP),

negative-interest rate policy (NIRP), unlimited credit lines, unlimited

liquidity, the purchase of trillions of dollars of assets, etc.

But what if the current

speculative credit bubbles in junk bonds, stocks and other assets don't crash

into crisis? What if they deflate slowly, losing value steadily but

with the occasional blip up to signal "the Fed has our back" and all

is well?

A slow, steady decline is

precisely what we can expect in an era of credit exhaustion, which I've covered

recently: ( The Coming Global Financial Crisis: Debt Exhaustion).

The central bank "solution" to runaway credit expansion that flowed

into malinvestment was to lower interest rates to zero and enable tens of

trillions in new debt. As a result, global debt has skyrocketed from $84

trillion to $250 trillion. Debt in China has blasted from $7 trillion 2008 to

$40 trillion in 2018.

A funny thing happens when you

depend on borrowing from the future (i.e. debt) to fund growth today: the new debt no

longer boosts growth, as the returns on additional debt diminish. This leads to

what I term credit/debt

exhaustion: lenders can no longer find creditworthy borrowers, borrowers

either don't want more debt or can't afford more debt. Whatever credit is

issued is gambled in speculations that the current bubble du jour will continue

indefinitely-- a bet guaranteed to fail spectacularly, as every speculative

credit bubble eventually implodes.

As expanding credit no longer

generates real-world growth, growth slows.Over time, marginal borrowers default as

revenues and profits erode, and this triggers a corresponding erosion in

employment and wages.

This erosion is so gradual, it

doesn't qualify as a crisis, and therefore central banks can't unleash

crisis-era fixes. Not only do they lack the political will to launch extreme

policies in a moderate decline, it would be unwise to empty the tool bag of

extreme fixes at the first hint of trouble; what's left for the crisis to come?

Even worse,

if the extreme policies fail to restore rapid growth and more importantly,confidence in future rapid

growth, then ramping up extreme

policies will be correctly interpreted as the desperate acts of clueless

authorities. This will crush confidence and trigger the very crisis the

authorities sought to forestall.

There are no extreme "fixes"

to secular declines in sales, profits, employment, tax revenues and asset

prices. Moderate

stagnation will not be reversed with moderate fixes (lowering interest rates a

quarter of one percent, etc.), and any attempt to institute extreme policies

will expose authorities' desperation right when confidence is vulnerable to

collapse.

The Fed and

other central banks are trapped in more ways than one.

THREE

NOTES OF NOTE:

1. I just added a new benefit for all subscribers/patrons: a

monthly Q&A where I respond to your questions/topics. You get other

exclusive benefits with a $1, $5 or $10/month patronage via patreon.com.

2. Resistance, Revolution,

Liberation: A Model for Positive Change is on sale this month: $4.95

Kindle edition, $9.95 print edition, a 33% discount.

3.

Did you know there are 3 new audiobooks available now?

Inequality and the Collapse of Privilege

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic ($6.95 ebook, $12 print, $13.08 audiobook): Read the first section for free in PDF format.

My new mystery The Adventures of the Consulting Philosopher: The Disappearance of Drake is a ridiculously affordable $1.29 (Kindle) or $8.95 (print); read the first chapters for free (PDF)

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic ($6.95 ebook, $12 print, $13.08 audiobook): Read the first section for free in PDF format.

My new mystery The Adventures of the Consulting Philosopher: The Disappearance of Drake is a ridiculously affordable $1.29 (Kindle) or $8.95 (print); read the first chapters for free (PDF)

My

book Money and Work Unchained is now $6.95 for the Kindle

ebook and $15 for the print edition. Read the first section for free in PDF format.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com. New benefit for subscribers/patrons: a monthly Q&A where I respond to your questions/topics.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com. New benefit for subscribers/patrons: a monthly Q&A where I respond to your questions/topics.